Decentr Announces the Launch of Our Beta Unbanked dLoans Pilot in South America

We are incredibly proud to announce the beta launch of our first dLoans product, called dP2P; a peer-to-peer (P2P) lending platform serving the unbanked and undocumented in South America. This is an important step towards our wider goals of implementing users’ ‘Personal Data Value’ (PDV) as a way to save when using our dPay services (including interest rates for borrowers on dP2P) by leveraging user data as economic value, all while helping users build their credit score online. This is achieved by users owning and controlling their ‘digital footprint’ on-chain as part of their DecID.

Unparalleled $DEC Utility

Critically, dP2P will create added utility for the $DEC token as all loans will be taken out and repaid in DEC via the Decentr dP2P feature on the Decentr platform, with all associated fees being paid in DEC. This is consistent with the Defi layer we are creating for Web3 whereby access to dPay and other Defi features is exclusively via the DEC token.

Financial Inclusion

We are proud to be launching our dLoans pilot in conjunction with 10-times published economics author and university lecturer, Professor John C. Edmunds. With a distinguished career teaching economics at prestigious universities including the Instituto de Empresa in Madrid, Spain and INCAE in Central America, John is incredibly impressed with our radical economic model, ‘deconomics’. John recognised that there is only one truly decentralised ‘Defi’ feature that yet exists, and that is PDV.

John is excited to join Decentr in an advisory capacity as he sees the potential for deconomics (‘decentralised economics’) and dPay to offer an economic system that, as he describes it: ‘Operates above the level of nation states’. This is critical to what both Decentr and John aim to achieve as regards promoting financial inclusion and equality — not only in Peru (where we have launched our beta dP2P) and the wider region, but the US and globally as well — all while protecting user identity, autonomy and data sovereignty in line with data protection laws.

Decentralised P2P Lending

Our first dLoans product is based on P2P lending, meaning we provide a platform for borrowers to request loans and private lenders to loan to them. This is a proven model, such as Lendingblock, Prosper, Crowdcube and dozens of others. It is perfect for a startup loans operation as it reduces risk to the company and the lenders through diversification. The system becomes even more viable, commercially scalable and verifiable once it is on-chain, as with the Decentr model/platform.

The initial revenue model for dLoans is based on transaction fees. The validators collect fees for executing transactions. They pay some of the fees to cover their costs, and some to pay stakers, and they pay some of the fees to Decentr that pays salaries, occupancy costs etc, for the corporate entity.

The company would also earn income from the loans because of transaction fees. For making available the forum where borrowers meet lenders, the company charges fees. The company can also use some of its cash to participate in providing the money being loaned. For example, the company could promise to provide 10% of each of a set number of initial loans. This would not require much money, and the ROI would be very safe because the initial loans will demonstrate a very low default rate.

Valuing Loan Activity

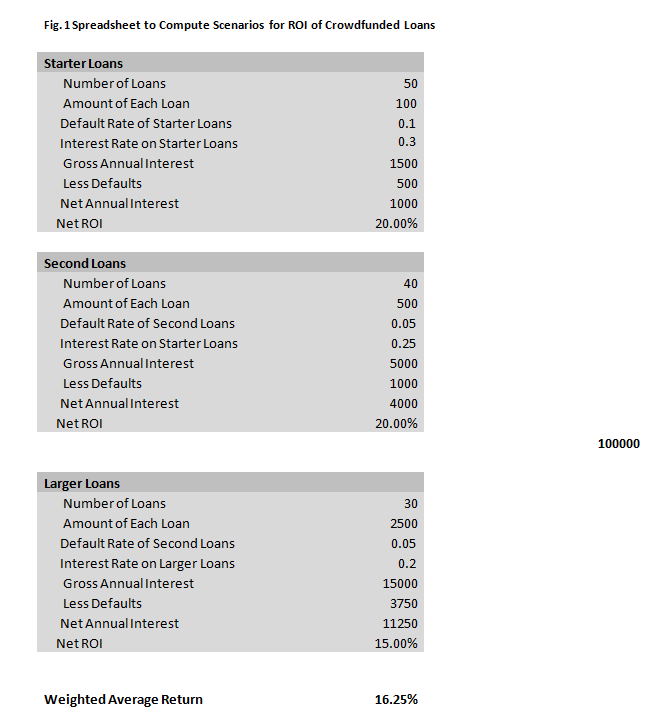

The loan activity is valued easily with a predictive spreadsheet (included below Figure 1) that illustrates the ROI on the loan portfolio after a specified number of loans of each magnitude.

We are looking at charging a 1% fee on each transaction associated with a loan. The $100 ‘starter’ loan will charge $1 from the lenders and $1 from the borrower, the 1% of the $9.60 monthly payment. All participants will willingly pay those fees, and understand why Decentr needs to charge them.

This visible, easily forecasted fee income is the lifeblood of financial services providers and will work even more efficiently on-chain.

Overall Loans Strategy

(As shown in Figure 1 below) the ROI will be 30% for the ‘starter’ loans, 25% for the second loans, then 20% for the third loans. The default rate will be zero in the rollout phase because all the borrowers will be computer savvy and crypto savvy, and selected by us in conjunction with our verification algorithms. After ‘civilian’ borrowers start to borrow, there will statistically be a predicted number of defaults (markedly less than with ‘paper’ applications), but not a significant amount, and this will all come under our risk assessment and AI/algorithmic verification procedures.

With regards to Peru and the wider region, our research shows that a ‘civilian’ borrower would only default after completely giving up hope of making a success of their dream of becoming an entrepreneur, prejudicing their online ID and ruling them out of more loans (and other financial products) in the future. They will quickly understand that Decentr/our loans portal is their only chance to get out of the disadvantaged situation they were born into.

After there are 50 or 100 loans that have been issued, it will be possible to package them into a portfolio. The portfolio would then earn an average return of the loans, net of defaults. It will probably yield about 20% in a stablecoin like USDC.

Once borrowers understand the way these loans work they will be good candidates for larger loans.

Spreadsheet:

Figure 1 (below) shows 50 “starter” loans, 40 second loans, and 30 larger loans. The average rate of return on those, assuming default rates, is 16.25%.

There is a way for an investor to get much higher ROI, and it is called securitisation. This would involve dividing the income from the loans, into a safe part and a risky part. The people who buy the safe part might make a return like 8% per year, and the people who buy the risky part might make 24% per year.

Suppose that the total amount of the loans is $100,000 and if there are no defaults then the loan book would yield 16% per year, per the spreadsheet below. If investors who provided $50,000 wanted safe income, that person might be guaranteed 8% a year. The investors who provide the other $50,000 would get the rest of the income. If no defaults, that would be 24%. The calculation is 50% at 8% + 50% at 24% = 100% at 16%. That structure of payments concentrates the risk, creating a senior bond and a junior bond.

It is important to note that loan repayments for users actually decrease over time as their PDV increases; in other words, the same data used for verification (as well as users’ online browsing data) is leveraged against user repayments, meaning user-borrowers are less likely to default for this reason. These decreases are not accounted for in the above figures as they will be minimal at first as users build their digital footprint.

Stay tuned for more details on dP2P features and launch dates. We will be conducting our closed beta for 2–3 months to acquire the data we need to feed back into development of our commercial product. We will keep you updated as we progress.

Official Links for Decentr:

Website: https://decentr.net

Twitter: https://twitter.com/DecentrNet

Telegram Group: https://t.me/DecentrNet

Telegram Ann: https://t.me/DecentrAnnouncements

Github: https://github.com/Decentr-net

Windows Browser: https://decentr.net/#download

OSX Browser: https://decentr.net/#download

Linux Browser: https://decentr.net/#download

Android Browser: https://play.google.com/store/apps/details?id=net.decentr.browser

iOS Browser: https://apps.apple.com/us/app/decentr-browser/id1609950309

Support (Validator, Staking, Browser Support): https://discord.gg/9cSxwKyEjR